We recently sat down with Rick Bonhof, a managing consultant who leads the Amsterdam regulatory change and compliance practice within the business consulting arm of Synechron—a leading digital transformation consulting firm that accelerates digital initiatives for banks, asset managers, and insurance companies around the world.

We recently sat down with Rick Bonhof, a managing consultant who leads the Amsterdam regulatory change and compliance practice within the business consulting arm of Synechron—a leading digital transformation consulting firm that accelerates digital initiatives for banks, asset managers, and insurance companies around the world.

In his role, Bonhof oversees a team of experts who help clients build the regulatory framework that enables compliance. As an advisor for the digital-first firm, Bonhof is hyperfocused on making compliance more efficient through the use of technology, leveraging emerging tech such as machine learning and existing systems such as GRCs.

Prior to Synechron, Bonhof served as a supervision officer for Dutch regulator Autoriteit Financiële Markten (AFM) at the height of the 2008 financial crisis. After spending seven years crafting and executing supervisory strategy for AFM, he decided to redirect his work from supervising firms to actually helping them become compliant with regulation. And so, after witnessing how Synechron helped a number of financial institutions get back on track with EMIR (the EU equivalent of Dodd Frank in the US), Bonhof transitioned to the firm.

During our sit-down, Bonhof shared his blended supervisory-consultative perspective on a variety of topics—from the role of regulatory change management during the COVID-19 pandemic to how Big Tech will shape the future of financial services.

Editor’s note: This interview has been lightly edited for clarity.

—

Setting the Record Straight on Regulators

Touching on his experience as a former regulator, Bonhof kicked off our conversation by sharing what he wished compliance professionals knew about regulators, and what he wished he had known as a regulator.

When I made the switch from regulator to consultant, I realized that a lot of financial firms are afraid of regulators. But the reality is that regulators are people too and most are not out to fine you. What I think compliance professionals sometimes forget is that if you’re able to explain to regulators why you made certain decisions and how you implemented certain requirements, they’ll listen to you.

“A lot of financial firms are afraid of regulators. But the reality is that regulators are people too and most are not out to fine you.”

My advice to compliance professionals is to document their interpretation of the rule and why they applied the rule in a certain way according to their interpretation, so they have all of the information they need when it comes time to talk to regulators.

On the flip side, what I wish I had known as a regulator was, no matter how simple a request for information may seem on paper, it doesn’t actually mean that there’s a clearcut way to gather requested information or to implement a new rule. Many financial institutions do not start out as multinational global-spending institutions—they grow through mergers, acquisitions, and restructuring.

So there’s a whole collection of teams that suddenly need to contribute to this “one simple request,” making it not so simple after all.

Managing Regulatory Change in the Time of COVID

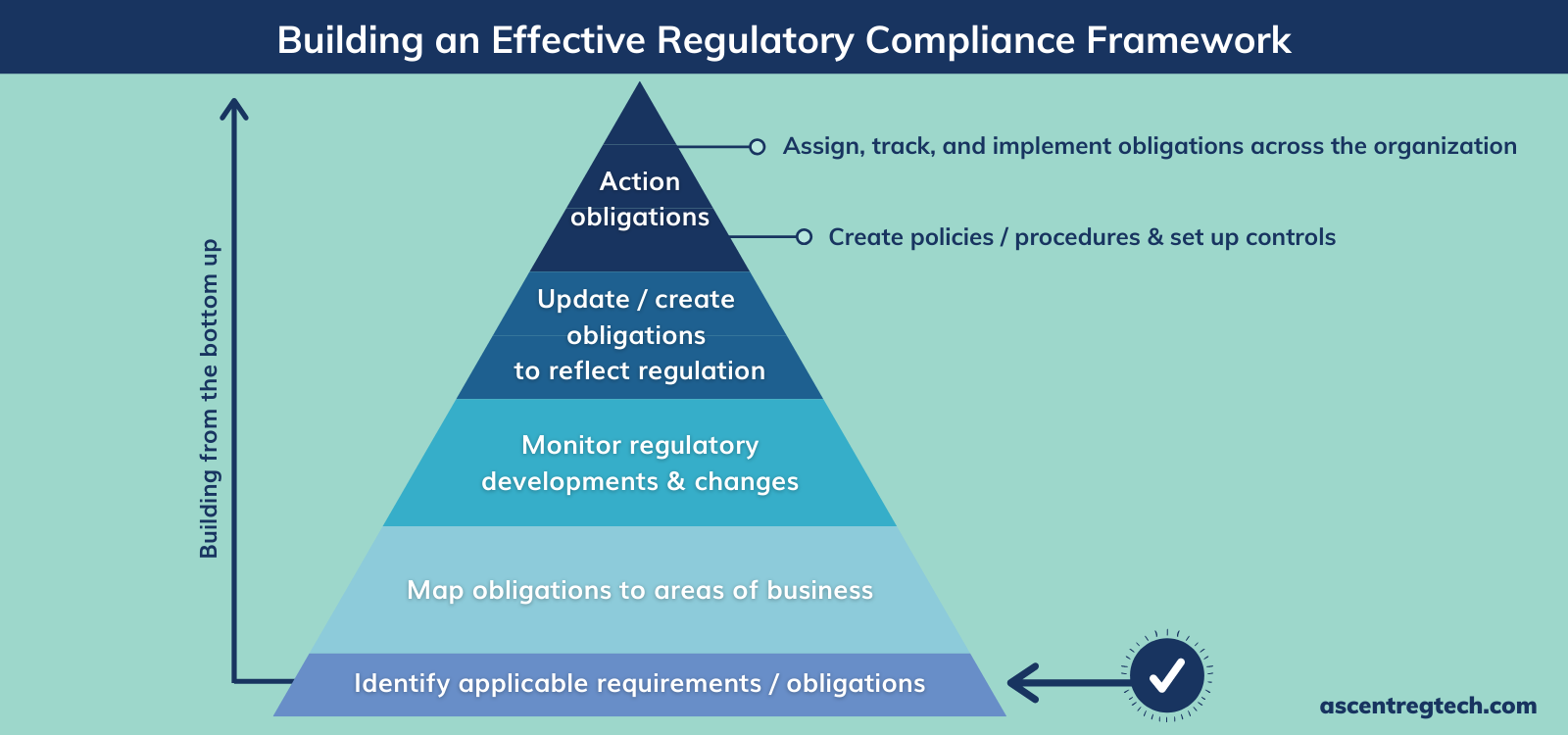

Bonhof has long emphasized the importance of having a well-documented regulatory change management (RCM) strategy, especially when it comes to major events such as financial crises, election years and of course — the COVID-19 pandemic.

When it comes to regulatory change management, my mantra has been “take control, be in control, and demonstrate control.”

“Take control” is about understanding what your obligations are, understanding the impact of them, and then implementing and enforcing a compliant process.

“Be in control” is about understanding where your firm is in terms of compliance with the requirements, and revisiting both its requirements and compliance processes frequently. You should not only be control testing your processes to understand whether your firm is compliant with existing rules, but also monitoring whether there’s a change coming that could impact compliance with those rules. And, if there is a change on the horizon, then you need to go back to “take control” and proactively act on it.

Lastly, “demonstrate control” is about being able to take the evidence that you have and explain both internally and externally to what extent you comply with those measures.

How to Avoid Dropping the Ball on RCM

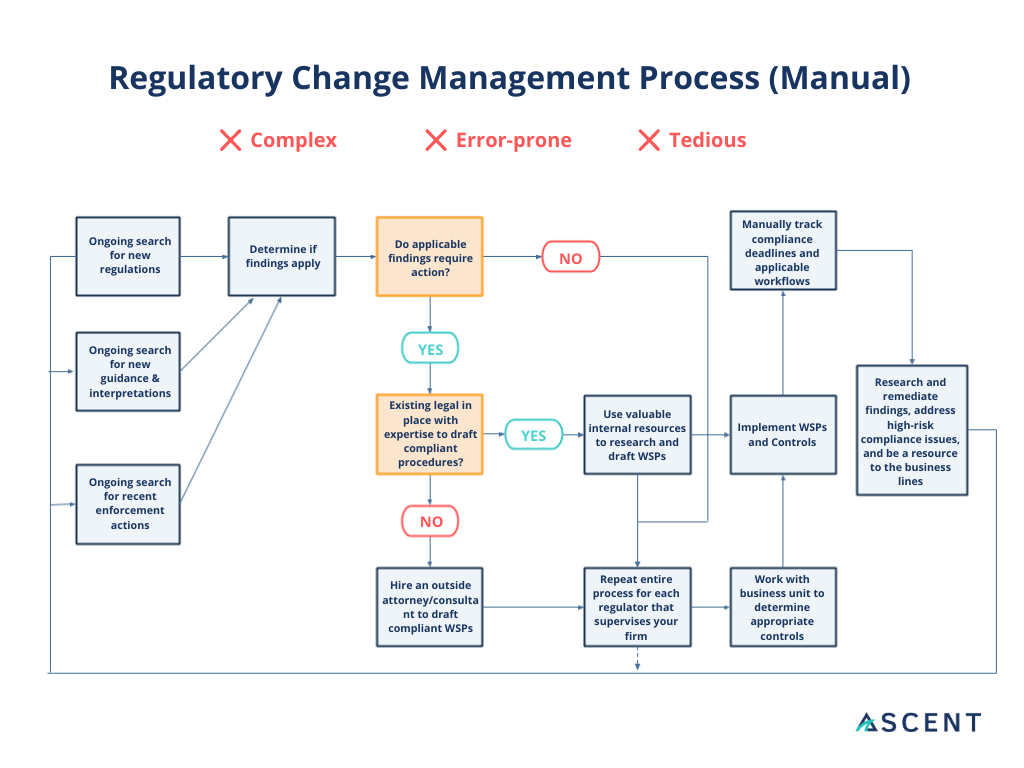

In Bonhof’s view, the biggest mistake that firms can make when implementing RCM best practices, is to treat them as a one-time solution.

Most regulatory change management processes are driven by a regulatory change implementation date. Let’s say that a firm has to comply with X, Y, and Z by January 1, 2021. What I’ve found (and even been guilty of myself) is that many firms focus solely on making that milestone without the end result in mind. So once the firm does reach it, everyone sort of drops the ball and says, “We’re done, we made it.” But that’s the wrong approach because 2021 does not mark the end of implementing that change, it actually marks the start of it.

What I’ve found (and even been guilty of myself) is that many firms focus solely on making [a] milestone without the end result in mind.

Firms are expected to be compliant with that new rule, and need to have a roadmap that accounts for what comes after that date. Firms often put makeshift technical solutions in place to meet the deadline, but then what happens is the technical solution silently becomes the structural solution. The result is that there’s no roadmap beyond that point to account for new data that needs to be tracked or changed, resulting in an issue of data quality and therefore explainability.

COVID Response: Swings of the Regulatory Pendulum

To Bonhof, regulatory change management has never been more important as the pandemic response continues to fold. While he and his team have seen the easing of certain regulatory requirements, they have also seen the mounting impact of others.

On the one hand, the regulatory response to the pandemic has been to suspend certain requirements in order to alleviate the burden of regulation. However, at the same time, we’ve also seen an increase in requests for financial firms to implement certain risk measures from regulators such as the European Securities and Markets Authority.

For example, we had an “intelligent lockdown” in the Netherlands that prohibited us from going to the shops or the cinema. As a result, this (like other lockdowns across the globe) had a large impact on service providers, as many businesses had outstanding loans with financial institutions and were suddenly not able to make good on those loans. This has led to a tipping of scales with regulators adding more capital reporting requirements, while continuing to suspend or delay implementation of other regulatory requirements. For example, ESMA deferred the final two phases of its bilateral margin requirements to provide additional operational capacity for counterparties to respond to the immediate impact of COVID-19.

On the Importance of Innovation in IRM

While regulators have been more forgiving during the pandemic, they have also become increasingly more aware of all of the possible gap—bringing the topic of Integrated Risk Management (IRM) to the fore. Here’s Bonhof’s take on IRM.

Integrated Risk Management allows you to identify what risks exist within your firm, define a response to those risks, and then determine whether your firm is within that risk appetite. Ultimately, IRM combines all of those processes and rolls them up into a multi-level process chart where you can prioritize risks and pinpoint which ones are of the highest risk to your firm.

IRM is such a hot concept right now because regulators are putting more emphasis on it.

As part of Synechron’s FinLabs RegTech accelerator suite, I’ve actually had the opportunity to work on automating parts of IRM. Knowing how effective your controls are is a key part of integrated risk management, so we built an intelligent control testing environment that maps a firm’s individual control statements into a decision tree that automatically runs against a data set to help firms quickly pinpoint whether a control is effective or not. This advancement frees up compliance teams’ valuable resources so they can focus on remediating any deficiencies.

These types of innovation are becoming more important as Integrated Risk Management continues to gain more traction. IRM is such a hot concept right now because regulators are putting more emphasis on it. For example, ESMA recently published a consultation paper that assessed the suitability of the management at financial institutions, which concluded that the highest levels of management (including at the board level) need to understand their firms’ requirements, how they are complying with them, and what the state of the firm’s risk management looks like.

Clash of the Titans: Big Banking vs. Big Tech

As an innovator in his own right, Bonhof is naturally drawn to industry disruptors. In particular, he has been following the rise of digital banks and believes that it’s only a matter of time until Big Tech enters into the banking industry as well.

The rise in digital banks has served as a catalyst for digital transformation in the industry at large. In order to stay competitive with digital banks, traditional banks have worked to provide digital services to their customers. For customers, having a digital bank account becomes more of a commodity because it opens up a whole ecosystem of additional services around it.

For digital banks, their competitive advantage is that they’re not burdened by a chain linked system of legacy tools or processes, so they can get it right immediately. Digital banks can be more nimble when it comes to things like digital client onboarding processes and company reporting. On the other hand, it’s difficult for digital banks to achieve the same scale as larger banks. Plus, they’re bound to face the same kind of regulatory requirements as incumbent banks and will need to comply with them, lessening some of their initial competitive edge.

When Big Tech enters the market, it will drive a significant change that some incumbent banks will likely not be able to transition through and will lose traction within the market.

What I’m really curious about is when Big Tech will officially enter into the banking space. Today, we have Apple Pay and Google Pay, but I think that it’s just a matter of time before they’re adding banking services to their offering. At that point the market will change. Digital banks just mark the beginning of the banking industry’s digital transformation. When Big Tech enters the market, it will drive a significant change that some incumbent banks will likely not be able to transition through and will lose traction within the market.

Financial Firms and Regulators to Step Up Their AI Game

With the high likelihood of Big Tech companies entering the market in addition to other innovations in financial services, Bonhof is encouraging the industry to direct its focus toward emerging technologies such as Artificial Intelligence (AI) now, before it’s too late.

I think regulators really need to step up their digital game. They need to understand the tech component that goes into digital banking. AFM just compiled an insightful trend report where they spoke around their fears about Big Tech entering into the financial market. Today, Big Tech is predominantly supervised by privacy watchdogs. But, if Big Tech entered the financial market tomorrow, financial market regulators would not always be allowed to share information with those supervisory agencies, so that would make supervision really difficult.

Regulators are just now issuing responses around the use of AI, which center around the concepts of explainability and trustworthiness. Together, they are two sides of the same coin because they help explain the decisions that come out of algorithms and apply fair principles that limit their biases. However, I still think that we have a ways to go and that regulation around the use of AI will only continue to increase in the future as the digital market matures.

The Role of AI in Regulatory Compliance

According to Bonhof, the role of AI is not just limited to the mechanics of digital banking. It applies to regulatory compliance too.

We recognize that regulators are starting to provide guidelines around AI, so we are changing the way that we advise our clients about AI. AI was once the new and exciting thing to talk about. Now it’s the means to an end. We’re looking at where AI models can help firms improve explainability in their compliance processes.

AI was once the new and exciting thing to talk about. Now it’s the means to an end.

Using robotics (or AI) helps automate certain regulatory compliance processes such as horizon scanning, and makes the outcomes of those processes more predictable and reliable. AI allows teams to focus less time doing the monotonous work of running these processes and more time on investigating outliers. Instead, the “robot” leads the processes and identifies areas where there are inconsistencies that require the review of compliance experts.

On Implementing RegTech: Final Advice

So, what’s Bonhof’s advice to firms that are looking to implement new technologies in their compliance programs? “Be really clear about what you want to achieve in your compliance program and therefore what you want the technology to achieve.”

First, you need to understand where you are and where you want to go. For instance, if your firm was just fined by a regulator, then you’ll likely need to find a solution that can help you become more compliant. On the other hand, if your organization is in a good place but needs to become more efficient, then it’s likely you’ll need a different tech stack than the firm that was recently fined. When you understand what you want to achieve by adding technology, then you can better pinpoint the right type of technology solution for your compliance program.

If you’d like to learn more about Synechron, visit their website. To learn more about Rick Bonhof, connect with him on LinkedIn.

If you’d like to contact an Ascent team member, you can do so here. Stay tuned for our next interview from the lines of defense. All interviews will be featured in our monthly Cliff Notes newsletter, which you can subscribe to below.

Subscribe to Cliff Notes